When it comes to eating out, Indians have lapped up Western QSR (Quick Service Restaurant) brands that focus on pizza, burgers, chicken-based food in a big way.

McDonald’s, KFC, Burger King, Domino’s, Pizza Hut, Subway, etc., are credible brands in this space, given that some of them entered India in the late 1990s (Domino’s, McDonald’s and Pizza Hut) and early 2000s (Subway and KFC).

Speak to any management, and they will cite secular trends of young population, rising urbanisation, growing affluence, accelerated shifts towards digitalisation and switch in favour of the organised sector for why you should be bullish.

However, if you go beyond these beaten-to-a-pulp words, investing in QSR stocks is not an easy meal. Valuations, for one, are expensive. Put together, the 5 main QSR stocks have a market value of ₹90,000 crore for churning out a meagre ₹650 crore profits on the back of ₹14,900 odd crore sales.

Undoubtedly, the last two-three years have witnessed a surge in interest around QSR stocks, with the recent pandemic-induced online ordering and delivery trend providing a boost. But divergent trends can be seen in the QSR stock universe in India.

Restaurant Brands Asia, formerly Burger King India, is up 113 per cent since its IPO in 2020. The stock of Devyani International (a franchisee of KFC and Pizza Hut) surged 135 per cent since IPO in 2021, but gains in Sapphire Foods (another franchisee of KFC and Pizza Hut) are lower at 25 per cent since its IPO in the same year. Among Indian QSR companies with long listing record, shares of Jubilant FoodWorks (master franchisee of Domino’s) are up 13 per cent on a 3-year basis, while Westlife Foodworld (owner-operator of McDonald’s restaurants) is up a whopping 2.5 times in the same period.To make better sense of this space, you need to understand the key dynamics at play for QSR stocks. Here they are:

Store-sales conundrum

Brick-and-mortar restaurants rely on physical stores to rake in revenue. The five major QSR companies together operate 4,600+ stores. Expanding QSR market opportunity and penetration beyond metros have driven QSR majors in India to undertake store expansion. For this article, we are focussing mainly on the India business for top QSRs as international segments are much smaller.

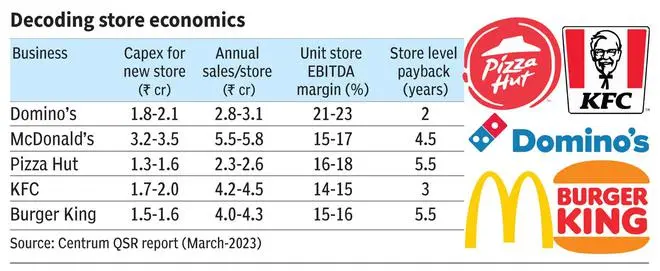

After the Covid-19 disruption, QSR chains continued their store additions at a brisk pace. But setting up stores requires money. Capex for each store ranges between ₹1.3 crore and ₹3.5 crore based on store size and location. Store rent as a percentage of sales ranges 8-15 per cent. However, average order value across brands is ₹450-600. Store sales don’t immediately start firing on all cylinders from day one. If a store doesn’t work, it is either rationalised or decommissioned (23 by Jubilant and 12 by Sapphire in FY22, for instance).

Store count growth doesn’t equal revenue growth for various reasons. Jubilant Foodworks, the most mature QSR play in India, grew store count by 10.3 per cent CAGR in FY20-23 period, but topline growth lagged at 9.2 per cent in the same period. Similarly, Devyani’s store count grew by 35.4 per cent CAGR while revenue grew by 25.4 per cent CAGR. However, some, like Westlife Foodworld, appear to have hit the right formula with controlled expansion. While Westlife grew store count by 4 per cent CAGR, sales advanced by 13.8 per cent CAGR.

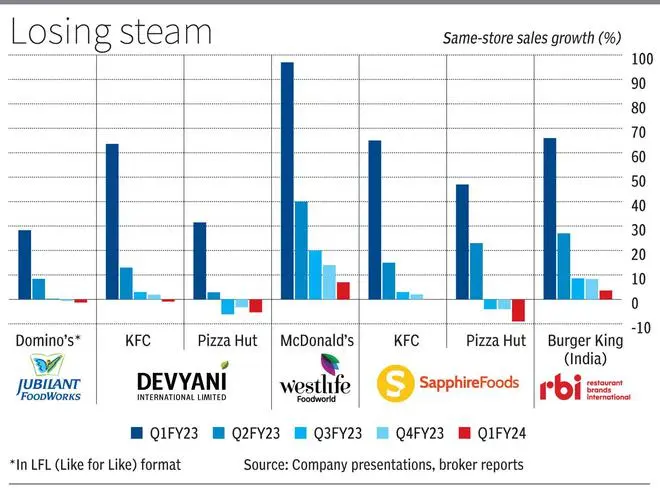

Investors should also note that a soft demand environment can impact store sales. In Q1 of FY24, same-store sales growth (SSSG) for most QSR majors has been negative, deteriorating from already poor rates in Q4 of FY23. Investors exhibit a preference for substantial growth in same-store sales. When a significant portion of a company’s revenue growth is attributable to the expansion of new stores, it may suggest that demand for the company’s products is plateauing. This, in turn, implies that minimal future revenue growth should be anticipated once the company attains saturation in terms of total number of locations.

Volatile margins

Despite the enthusiasm surrounding the high-growth Western QSR category, the valuation of companies operating within this domain may actually hinge upon their margin strategy. Gross margins in QSR stocks ranges at 65-75 per cent while EBITDA margins at 11-23 per cent. Store margins are closer to EBITDA margins. Net profit margins are lower (5 to 10 per cent), except loss-making Restaurant Brands Asia (FY23). Margin expansion in general is led by operating leverage, but what complicates the matter are the volatile margins.

The swing in margins could be due to many reasons, such as sticky input cost inflation. Cost-saving initiatives and pricing actions can only do so much. In fact, in most cases, QSR chains have to absorb inflation. In FY23, for instance, Jubilant Foodworks’ performance was a tale of two halves. Post the festival season, there was sudden deceleration in demand as rampant inflation started exerting pressure on discretionary consumption. In one year, cheese price increased 40 per cent, flour price 28 per cent, chicken and paper box prices 30 per cent. As a result, Jubilant’s operating profit margins — after being at 24 per cent for H1 of FY23 — slipped to 21.5 per cent in Q3 and further to 19.6 per cent in Q4.

Similarly, other QSRs saw inflation impact. For example, Devyani’s operating profit margin fell by 100 bps in FY23. In KFC, the main ingredients are chicken, oil, flour and packing material. Some stabilisation has been seen in them as well as in vegetables in Q1 of FY24, helping operating margin find base around 20 per cent. In case of Sapphire Foods, quarterly operating margins slid from 20 per cent plus to 17.5 per cent from Q1 to Q4 of FY23. In a recent conference call, Sapphire management reckoned that demand is expected to remain sluggish for at least a year before stabilising, as inflation moderates.

Dietary preferences also change, which impacts certain QSRs more than others. For instance, Q2 normally is seasonally the lowest quarter for chicken-based items. Typically, Shravan/Sawan period falls in this quarter, where a lot of Hindus turn vegetarian. Also, as companies compete in similar products (burgers and fried chicken), the rising share of value-for-money products does pose a risk for margins. Higher salience of low-ticket-value/low-margin products (for e.g. under ₹100 price tag) may bring volumes, but delay store payback periods. Overall inflationary trends, not just input prices, also force consumers to down-trade from premium-end burgers and pizzas. A changing mix impacts margins. So, investing in QSR stocks based on historical margin trends may be tricky.

E-ating out

While QSRs talk about omni-channel (dine-in, apps, online delivery, drive-thru, on-the-go) strategies, some key changes are happening. On-premise consumption is, of course, returning, but there is growing evidence of incremental occasions and habit-build in favour of off-premise eating. For Pizza Hut in India, off-premise sales accounted for 56 per cent of the total sales mix in FY23. For Westlife, overall contribution of the off-premise business to the topline is 40 per cent (Q1FY24).

The Y-o-Y growth of Indian online food delivery market in the last three years is 100 per cent. Statistics show the overall share of online sales in food service industry has reached double digits (10.7 per cent) in 2021 vs low single-digit (1.9 per cent) in 2016, according to Euromonitor. Pre-Covid, this was 4.3 per cent. Consumers are now accustomed to ‘delivery-across-town’ classification, helped by the ever-expanding reach of the delivery ecosystem in Tier II/III/IV. Due to the recent pandemic, standalone stores with a strong emphasis on dine-in services have been disproportionately affected. This could indicate a potential shift in the market towards delivery-centric business models, which has a bearing on how QSR companies perform in future. So, store-led growth strategies may need to be re-calibrated. Close to half restaurants pay in excess of 20 per cent of each order as commission (gross take rate). Note premium restaurants pay lower median take rates.

For instance, Devyani (KFC and Pizza Hut) has increased focus on smaller-sized, delivery-focussed stores vis-à-vis larger dining-oriented stores in India. To serve online deliveries, QSRs will actively invest in cutting-edge technology to enhance digital capabilities, improve delivery efficiency and optimise overall operations. Similarly, omni-channel strategy enabled a reduction in the size of restaurants by 45 per cent for Sapphire (another operator of KFC and Pizza Hut outlets).

The acceleration of the growth of online through delivery apps has led to prominence for ‘cloud kitchens’ where food is prepared as ‘made to order’ suiting consumer taste and preference, but prices are still affordable. While cloud kitchens started to gain traction way back in 2015, thanks to Covid ‘cloud only’ food service brands and businesses received a boost in popularity. The concurrent rise of food aggregators also supported this growth.

While cloud kitchens in the online playground are tough competitors, lack of physical brand connect with the customer, low entry barriers leading to a crowded ecosystem with high mortality rate, and lack of reach outside of Tier-I cities are their disadvantages. But if Zomato and Swiggy aggregator ecosystems thrive, customer connect, coupled with subsidised delivery costs and discounts/promotions, can pose a threat for QSRs. Rebel Foods is the largest cloud kitchen which has displayed successful scale-up in recent times. Indirect competition from aggregators on private label food brands can also increase rivalry in QSR online sales segment.

Valuations and growth expectations

Given that QSRs are linked to consumption, QSR stocks are undoubtedly pricey. Compared to Nifty 50’s 1-year forward price to earnings of 22 times, the forward PE of QSR stocks ranges at 70-100 times Given the capital-intensive nature of QSRs, even on the EV/EBITDA valuation multiple these stocks trade at 19-34 times for FY24 and 15-28 times for FY25, which is expensive.

Despite muted demand and lower-than-expected new-store openings in Q1 of FY23, companies have retained annual store-opening projection for FY24 (Jubilant: 200-225, Devyani: 275-300, Westlife: 40-45, Sapphire: 130-160 and Restaurant Brands: 50 (India)). These could be at risk.

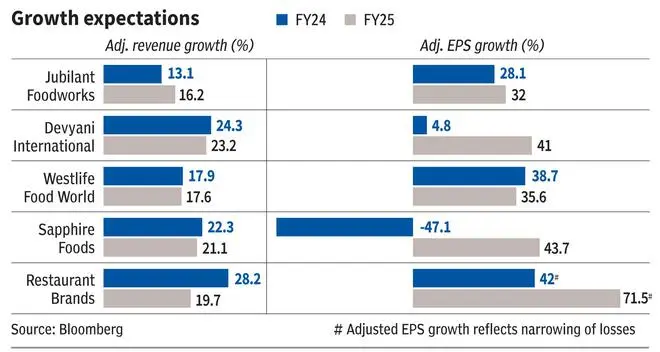

Despite Bloomberg consensus estimate cuts to FY24 and FY25 earnings (compared to January-2023 projections), QSR stocks, viz. (Jubilant & Sapphire, up 19 per cent, Restaurant Brands, 26 per cent, Devyani, 44 per cent and Westlife 46 per cent) have participated in the broader market rally since March 2023 lows.

At least in the short term, pizza players such as Jubilant are expected to grapple with weak demand, incremental competition, and rising inflation in dairy. These have driven analysts to expect modest growth in their toplines. For pizza and chicken-food players (Devyani and Sapphire), these challenges hold true, along with rise in chicken prices, but small price hikes are expected to help them defend margins while growing sales. Burger player Westlife Foodworld has been an outlier of sorts in recent times, given its strong SSSG (same-store sales growth) when peers have struggled. Payment of maiden dividend by the company has also been taken as a signal of management’s confidence about growth prospects.

![]() Comments

Comments